JATO Dynamics data for 28 European markets indicated that April was largely a positive month for Europe’s new passenger car market. While EVs, SUVs and Chinese-made cars have been the main drivers of growth in recent years, JATO’s latest monthly data reveals that this is no longer the case. In April, the market share of battery electric vehicles (BEVs) increased by just 0.3 percentage points – from 13.1% in April 2023 to 13.4% last month – while monthly registrations for the category rose by 15%. Although this figure is higher than the year-on-year growth of the overall market, it is markedly lower than the monthly increases recorded last year, JATO said.

A total of 1,080,517 new vehicles were registered during the month, an increase of 12.6% compared to April 2023, driven largely by demand for B-hatchbacks and compact cars. Year-to-date figures show that a total of 4,461,734 new units have been registered so far in 2024, a rise of 6.7% on the same point last year.

“The electric car market is not performing as well as it was this time last year,” Felipe Munoz, global analyst at Jato Dynamics said. “This is largely due to the ongoing price cuts which has raised concerns among consumers over the residual value of EVs and uncertainty as to how prices will evolve in the coming months.”

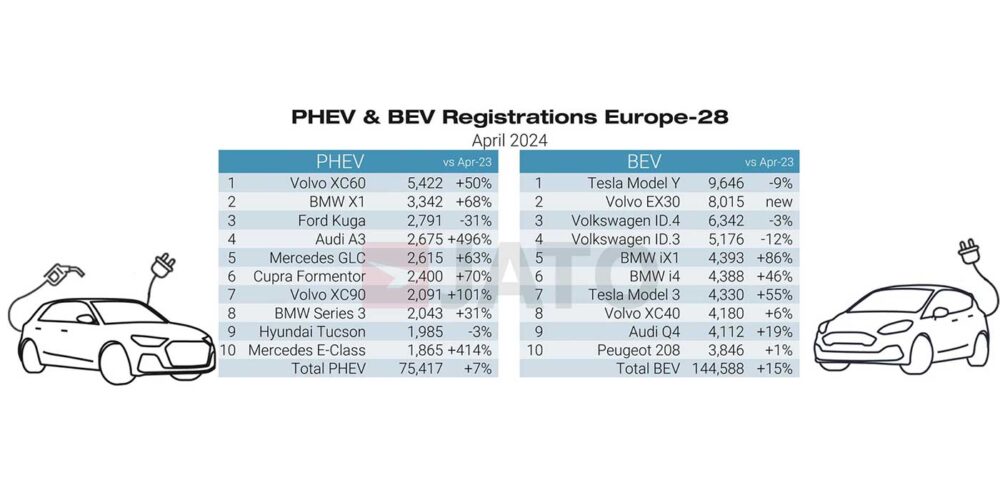

Volkswagen dominated the BEV market in April, despite recording a 7% decline in volumes compared to the same month last year, JATO data found. Tesla followed closely with a 0.6% growth in registrations, with the Model Y maintaining first place in the ranking for BEV models.

However, BMW was the main driver of growth in April, with registrations of its electric models soaring 82% year on year. The German manufacturer registered 14,179 units over the month – just 28 units less than Tesla. Volvo also performed well with 13,275 units registered, marking a 141% increase from April 2023. This was largely due to strong demand for the Volvo EX30, Europe’s second-best-selling BEV during the month, according to JATO data.

In April, BYD registered 2,746 units, outpacing the likes of Cupra, Nissan and Toyota to become the 15th best-selling brand in the BEV rankings. Meanwhile, OEMs that saw a decline in registrations of electric models last month include Opel/Vauxhall (-37%), Polestar (-26%), Skoda (-13%) and MG (-12%).

Despite the success experienced by BYD in April, Chinese-made cars are yet to become a major force in Europe. The overall market share of Chinese car brands in Europe rose from 2.22% in April 2023 to 2.35% in the same month this year. MG accounted for 68% of the 25,360 total units registered by Chinese brands during the month, JATO said.

“Although there is lots of noise around the arrival of Chinese car brands in Europe, they are still something of a rarity – evidenced by the slow uptick in registrations over the past year,” Munoz noted. “MG, a brand that many still associate with the West, accounted for two in three registrations of Chinese-made vehicles.”

“The continued inability of Chinese-made vehicles to truly penetrate Europe’s automotive market could be a result of the ongoing perception issues that Chinese OEMs face, particularly in light of negative attention from the European Commission’s investigation. However, Chinese-made cars continue to prosper in the BEV market with a market share of 6.6%,” he said.

Despite their historical popularity with consumers, JATO data found that the market share of SUVs dropped from 51.3% in April 2023 to 51.1% in April. SUV registrations only increased by 12% year on year, lagging the growth of the overall market over the same period.

Within the SUV segment, Audi, Ford, Kia, Renault and Skoda struggled in April, whereas BMW, Hyundai, Mercedes, Toyota, Volkswagen and Volvo all gained market share.

Read the full article here